Discover why retirees with $1M+ saved choose flat-fee financial advice over the 1% AUM model. Learn how Ignite Financial’s transparent approach could help you cut costs, lower taxes, and retire with confidence.

Last updated: May 2026 · Written by Casey Redmond, CFP® · Ignite Financial, Cedar Falls, Iowa

A flat-fee financial advisor is a fiduciary planner who charges one transparent, predictable annual fee for comprehensive financial planning and investment management — regardless of your portfolio size. Unlike AUM advisors who take a percentage of your assets every year, or commission-based advisors paid by the products they sell, a flat-fee advisor's only incentive is to serve your goals.

If you've spent 30+ years building your retirement savings, the last thing you should be doing is quietly handing tens of thousands of dollars a year to your financial advisor — with fees that grow automatically every time your portfolio does.

That's exactly what happens under the traditional 1% AUM model. And for retirees with $1 million or more saved, the difference between that model and flat-fee planning can be staggering.

Our flat-fee approach is designed for people who want clarity, transparency, and comprehensive guidance in or near retirement. You're likely a strong fit if you:

If you're looking for hot stock tips or short-term trading strategies, we're probably not the right fit — and we'll tell you that upfront.

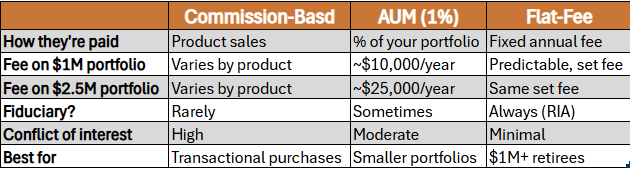

Most advisors charge in one of three ways:

With a flat fee, you know exactly what you’re paying—no surprises, no percentages.

Commission-based: The advisor earns a percentage of the financial products they sell you. An annuity sale on $500,000, for example, can generate a commission of $30,000–$40,000 — paid whether or not it was the right choice for your plan.

AUM (Assets Under Management): You pay a percentage of your portfolio each year, typically around 1%. The fee rises automatically as your investments grow — even if your financial situation hasn't gotten more complex.

Flat fee: You pay one predictable annual fee tied to the complexity of your situation, not the size of your accounts.

At Ignite Financial, we work exclusively on a flat-fee basis. One transparent fee. No percentages. No commissions. No surprises.

The math here is worth sitting with for a moment.

With 1% AUM:

And that fee doesn't decrease because your needs simplified. It rises with every dollar of investment growth — whether or not your financial plan changed at all.

With a flat fee:

Your cost reflects the work required, not your account balance. Whether your portfolio is $1M or $5M, your fee reflects the complexity of your situation — not a percentage of everything you've worked to build.

For retirees who have saved diligently, that's a meaningful difference.

How an advisor gets paid shapes the advice they give, whether they intend for it to or not.

Commission example: An advisor recommends putting $500,000 into an annuity. At an 8% commission, that's $40,000 paid to them upfront. The incentive is the sale — not your long-term income plan.

AUM example: You have $1.5 million under management at 1%, so you're paying $15,000 a year. You want to withdraw $500,000 to buy a vacation home. Your advisor's annual fee just dropped by $5,000. Even the most well-intentioned advisor may — consciously or not — find reasons to talk you out of it.

Flat-fee example: Your fee is tied to the complexity of your financial life. Pulling $500,000 for a vacation home doesn't change what we're paid. Our only job is to help you make the best decision for your goals.

At Ignite, we go beyond spreadsheets. We help you:

Here’s what our client experience looks like:

This isn’t cookie-cutter. It’s personal, proactive, and designed to give you clarity for decades to come.

Here’s what’s included in our flat fee service—so you know what’s covered, without surprises. We help you make confident decisions across every aspect of your financial life:

All clients receive complimentary access to create or update a will, advance directive, power of attorney, and a revocable trust. We also provide a binder and help you organize everything in one place.

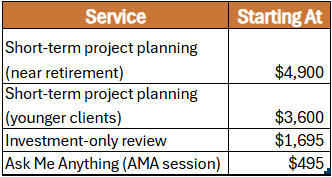

Our comprehensive planning and investment management services typically range from $8,000 to $14,000 per year, with most clients between $9,000 and $12,000 depending on the complexity of their situation. This includes both ongoing financial planning and investment management.

We also offer focused engagements for those who aren't ready for comprehensive planning:

No commissions. No percentages. One flat, transparent fee.

Our flat-fee approach is designed for people who want clarity, transparency, and comprehensive guidance in or near retirement. We’re the best fit if you:

Our goal: help you reduce lifetime taxes, improve your investments, and maximize your retirement income—with peace of mind.

We’re not the right fit if you’re looking for hot stock tips or short-term trading strategies.

If you're 50 or older, have $1 million or more saved, and want a clearer path through retirement — let's talk.

In a free introductory call, you'll get a straightforward assessment of where you stand, honest answers to your most pressing retirement questions, and a clear sense of whether we're the right fit for each other.

No pressure. No sales pitch. Just clarity.

Ignite Financial is a flat-fee, fee-only fiduciary firm based in Cedar Falls, Iowa, serving families locally in the Cedar Valley and virtually across the United States. Casey Redmond, CFP® and Mike Dunlop, CFP® are co-founders.

What is a flat-fee financial advisor?

A flat-fee financial advisor charges one predictable annual fee for comprehensive financial planning and investment management — regardless of your portfolio size. Unlike AUM advisors who take a percentage of your assets, a flat-fee advisor's cost is based on the complexity of your situation. This structure eliminates the conflict of interest that exists when an advisor's income grows every time your portfolio does.

Is flat-fee better than 1% AUM for retirees?

For retirees with $1 million or more saved, flat-fee planning is almost always more cost-effective than 1% AUM — and better aligned with your interests. At $1M, 1% AUM costs $10,000/year. At $2.5M, it's $25,000/year. A flat fee stays predictable regardless of portfolio growth, and your advisor has no financial incentive to discourage withdrawals for things like a vacation home, gifting to family, or paying off a mortgage.

How much does a flat-fee financial advisor cost?

At Ignite Financial, comprehensive planning and investment management typically ranges from $8,000 to $14,000 per year, with most clients between $9,000 and $12,000. We also offer project-based planning starting at $4,900 and an Ask Me Anything session for $495. There are no commissions, no hidden fees, and no percentage of assets.

Is a flat-fee advisor a fiduciary?

Yes — flat-fee advisors who are registered investment advisors (RIAs) are legally required to act as fiduciaries at all times, meaning they must always put your best interest ahead of their own. At Ignite Financial, we are a fee-only fiduciary firm. We have signed a fiduciary oath and never accept commissions of any kind.

What's the difference between flat-fee and fee-only?

"Fee-only" means the advisor is paid exclusively by their clients — no commissions, no third-party payments of any kind. "Flat fee" describes the structure of that payment: one predictable annual amount rather than a percentage of assets. Ignite Financial is both fee-only and flat-fee.

Do you work with clients outside of Cedar Falls, Iowa?

Yes. While we're based in Cedar Falls and serve many families across the Cedar Valley — including Waterloo, Iowa City, and the broader Cedar Falls area — we work virtually with clients across the United States.

What if my financial situation changes after I become a client?

Plan updates are included in your flat fee. Whether it's an inheritance, property sale, early retirement, or unexpected transition — we adjust your plan proactively. We revisit fees every two years, typically adjusting only for inflation.

Can you work with my CPA or estate attorney?

Yes. We coordinate directly with your tax preparer, CPA, and estate attorney as part of your plan at no additional cost.