Fee-only financial planning is a compensation model in which a financial advisor is paid exclusively by their clients — through flat fees, hourly rates, retainers, or a percentage of assets — and accepts no commissions, no referral fees, and no payments from financial product companies of any kind.

Last updated: May 2026 · Written by Casey Redmond, CFP® · Ignite Financial, Cedar Falls, Iowa

If you're approaching retirement with $1 million or more saved, understanding this distinction could be one of the most financially significant decisions you make.

Your advisor just recommended an annuity. Or a specific mutual fund. Or a life insurance policy wrapped inside your investment account.

The question worth asking: Was that the best option for you — or the one that paid them the most?

The answer often comes down to one thing: how your advisor gets paid.

Not all financial advisors are paid the same way. Understanding the difference could save you thousands of dollars — and protect you from advice that quietly benefits your advisor more than it benefits you.

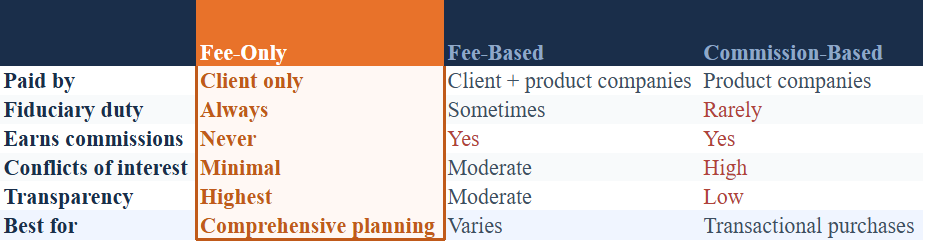

1. Commission-Based

These advisors are paid by the financial products they sell you. Every annuity, mutual fund, or insurance policy they recommend generates a commission — sometimes a substantial one. A common annuity commission, for example, can run 6–8% of the amount invested. On a $500,000 purchase, that's $30,000–$40,000 paid to your advisor upfront, regardless of whether the product was the best fit for your situation.

2. Fee-and-Commission (Also Called "Fee-Based")

These advisors charge you a direct fee and earn commissions on products they sell. The name sounds similar to "fee-only," but it's meaningfully different. The hybrid model still creates built-in conflicts of interest — because every product recommendation carries a potential paycheck. Under the SEC's Regulation Best Interest (Reg BI), broker-dealers must act in your best interest at the point of a recommendation — but this standard is weaker than the ongoing fiduciary duty that governs registered investment advisors (RIAs).

3. Fee-Only

Fee-only advisors are compensated exclusively by their clients — through hourly rates, flat fees, retainers, or a percentage of assets managed. They accept no commissions, no referral fees, and no payments from financial product companies. Their only financial incentive is to serve you well.

Here's the honest reality: advisors who earn commissions aren't necessarily bad people. But the compensation structure creates a conflict that's difficult to ignore.

When your advisor earns more by recommending Product A over Product B — even if Product B is cheaper and better suited to your goals — they face a choice between their interests and yours. Some advisors navigate that well. Many don't. And even well-intentioned advisors can unconsciously steer toward higher-paying options without realizing it.

This is why the distinction between "suitable" and "in your best interest" matters so much:

Fee-only advisors who are registered investment advisors (RIAs) operate under the fiduciary standard at all times. Commission-based and fee-and-commission advisors often do not.

Fee-only financial advisors may be compensated in several ways:

At Ignite Financial, we work exclusively on a flat-fee basis — one transparent annual fee that covers everything from retirement income planning and investment management to tax strategy, insurance review, and estate planning. No commissions. No percentages that grow with your portfolio. Just straightforward advice aligned entirely with your goals.

We serve clients in Cedar Falls, Iowa, across the Cedar Valley, and virtually throughout the United States.

The National Association of Personal Financial Advisors (NAPFA) is the leading professional organization for fee-only financial planners in the United States. NAPFA's position is that fee-only compensation is the most transparent and objective method available, minimizing conflicts of interest and ensuring advisors operate as true fiduciaries. All NAPFA members are required to work exclusively within the fee-only structure and may not accept commissions for their work.

You can verify whether a financial advisor is truly fee-only by searching the NAPFA member directory or by asking them directly to sign a fiduciary oath — a written commitment to always act in your best interest.

If you're approaching retirement with $1 million or more saved — whether in 401(k)s, IRAs, brokerage accounts, or Iowa farmland — how your advisor is paid can have a dramatic impact on your long-term financial outcomes. A single unsuitable annuity recommendation — driven by commission rather than your needs — could lock up your assets, limit your flexibility, and cost you significantly in fees and lost growth over time.

Fee-only planning removes that conflict entirely.

If you're 50 or older and want advice you can trust — advice built around your retirement, not your advisor's compensation — we'd love to talk.

Schedule a free call with Ignite Financial →

What is the difference between fee-only and fee-based?

Fee-only advisors are paid exclusively by their clients and never earn commissions. Fee-based advisors charge clients a direct fee but also earn commissions on products they sell. Despite the similar names, fee-based advisors still have inherent conflicts of interest that fee-only advisors do not.

Is a fee-only financial advisor a fiduciary?

Yes — fee-only advisors who are registered investment advisors (RIAs) are legally required to act as fiduciaries, meaning they must always put your best interest ahead of their own. This is a higher and more consistent standard than what applies to commission-based or broker-dealer advisors under Regulation Best Interest.

How much does a fee-only financial advisor cost?

It depends on the fee structure. Hourly advisors may charge $200–$500/hour. AUM advisors typically charge 0.5–1.5% of assets annually. Flat-fee advisors (like Ignite Financial) typically charge $8,000–$14,000/year for comprehensive planning and investment management — a predictable cost that doesn't rise automatically with your portfolio.

How do I know if my advisor is truly fee-only?

Ask them directly: "Do you or your firm receive any compensation beyond what I pay you — including commissions, revenue sharing, or referral fees?" You can also search the NAPFA member directory, check their SEC ADV Part 2 disclosure document, or ask them to sign a written fiduciary oath.

What does NAPFA stand for?

NAPFA stands for the National Association of Personal Financial Advisors. It is the largest professional organization in the United States dedicated exclusively to fee-only financial planning. All NAPFA members must adhere to a strict fee-only compensation standard and fiduciary pledge.

Is fee-only financial planning available in Cedar Falls, Iowa?

Yes. Ignite Financial is a fee-only, flat-fee fiduciary firm based in Cedar Falls, Iowa. We serve families locally in the Cedar Valley and virtually across the United States. If you're looking for a fee-only financial advisor in Iowa — whether near Cedar Falls, Cedar Rapids, Waterloo, or elsewhere — we'd be happy to talk.

Ignite Financial is a flat-fee, fee-only fiduciary firm serving clients in Cedar Falls, Iowa and across the United States. Casey Redmond, CFP® and Mike Dunlop, CFP® are co-founders.